flowchart TD

A[Get a good idea<br/>literature or industry] --> B{Feasibility:<br/>interesting? story?<br/>audience? opp. cost?}

B -->|yes| C[Resist the literature<br/>re-derive independently]

C --> D[Build simplest model<br/>1 period, 2 products,<br/>linear utility]

D --> E[Generalize:<br/>add complexity<br/>one assumption at a time]

E --> F[Search the literature:<br/>why didn't I do<br/>what they did?]

F --> G[Seminar:<br/>stress-test assumptions]

G --> H[Write the paper]

31 Analytical Models

Marketing science advances along two complementary tracks. Analytical models reason about markets through pure mathematics: a researcher posits an environment of consumers and firms, assumes that each agent optimizes, and derives the behavior that must follow in equilibrium. Empirical models instead let data speak, estimating relationships and testing the predictions that theory hands them. This chapter is about the first track—how to build a stylized mathematical world, solve it, and extract substantive claims about pricing, positioning, advertising, channels, contracts, and the diffusion of new products—while keeping one eye on the empirical counterparts that make the theory testable.

A model, in the working definition that organizes the field, is a representation of the most important elements of a perceived real-world system. The art lies in the word important: a model that retains everything is the territory, not the map, and a model that retains too little predicts nothing. The discipline of marketing modeling is therefore the discipline of principled omission. The reward for doing it well is decision-relevant insight. Little (1976) frames the goal as a decision calculus—“a model-based set of procedures for processing data and judgments to assist a manager in his decision making”—and argues that such a system earns managerial adoption only when it is simple, robust, easy to control, adaptive, as complete as possible, and easy to communicate with. Those six criteria recur throughout this chapter as a standard against which competing formulations are judged: a more elaborate model that a manager cannot interrogate is often a worse model.

By the end of the chapter the reader should be able to classify a marketing problem by the type of model it calls for, set up the corresponding game or optimization, solve for equilibrium or the optimum, and state the assumptions whose failure would overturn the result. We proceed from the philosophy and craft of model building, through the workhorse spatial and oligopoly models, to the major application domains—market response, channels, advertising, product quality under asymmetric information, bargaining, search-theoretic pricing, promotions, salesforce compensation, and diffusion—closing with the optimization models that turn behavioral theory into resource-allocation decisions.

31.1 A Taxonomy of Marketing Models

Marketing models improve decision-making in three broad families, and it is worth fixing the distinctions before building anything, because the family determines what counts as a valid test of the model.

Econometric models describe, predict, and simulate. A descriptive model summarizes how a market behaves; a predictive model forecasts an outcome such as sales; a simulation model traces how the system responds to a counterfactual intervention. Leeflang et al. (2000) organizes the empirical tradition along exactly these lines. Predictive models include sales models built on time-series data, trial-rate models built on exponential growth, and the new-product growth model of Bass (1969). Descriptive models include purchase-incidence and purchase-timing models built on the Poisson process, brand-choice models built on Markov or learning processes, and pricing models for oligopolistic markets in the tradition of Howard and Morgenroth (1968). Normative models, by contrast, prescribe: they maximize an objective such as profit over price, advertising, and quality, the program studied by Dorfman and Steiner (1976) and extended by Roberts, Ferber, and Verdoorn (1964) and Lambin (1970). The decision-calculus program of Little (1970) and the multinomial logit choice model brought to scanner data by Guadagni and Little (1983) are landmarks in turning normative structure into operational tools.

Optimization models take a market-response function—how outputs such as sales, share, profit, and awareness respond to inputs such as price, advertising, and selling effort—together with cost functions and constraints, and maximize an objective. The candidate decisions that such models automate are familiar from practice: promotion and pricing programs, media allocation, distribution, product assortment, and direct-mail solicitation. Quasi- and field-experimental analyses and conjoint and choice experiments complete the toolkit, supplying the causal variation that observational data often lack.

Cutting across these families is the distinction between decision-support modeling and theoretical modeling. The former describes how things work; the latter prescribes how things should work. Theoretical, game-theoretic models in the tradition of K. S. Moorthy (1993) are best understood as logical experimentation: the modeler specifies an environment through assumptions, deduces consequences, and learns which assumptions drive which conclusions. K. S. Moorthy (1993) separates two kinds of assumption that play very different roles. Mathematical assumptions are made for tractability and carry no empirical content; substantive assumptions encode claims about the world and are the proper object of empirical testing. A classic illustration is the design of a salesforce compensation package combining salary and commission, which K. S. Moorthy (1993) reads as a trade-off between insuring the salesperson against income risk and motivating effort—a substantive tension we return to in Section 31.16. The internal and external validity of such a model are questions about its boundary conditions, and Friedman’s dictum looms over the enterprise: theories are tested by their predictions, not by the realism of their assumptions.

Because so much of analytical marketing is game theory, it helps to organize the solution concepts by two attributes of the game: whether moves are static (simultaneous) or dynamic (sequential), and whether information is complete or incomplete. The four cells in Table 31.1 name the equilibrium concept that applies in each.

| Information | Static (simultaneous) | Dynamic (sequential) |

|---|---|---|

| Complete | Nash equilibrium | Subgame-perfect equilibrium |

| Incomplete | Bayesian Nash equilibrium (auctions) | Perfect Bayesian equilibrium (signaling) |

K. S. Moorthy (1985) supplies the vocabulary that the rest of the chapter assumes. Rationality is the maximization of subjective expected utility; intelligence is the recognition that rival firms are themselves rational and will reason likewise. The rules of the game comprise the number of firms, the feasible set of actions for each, the utilities attached to every combination of moves, the sequence of moves, and the information structure—who knows what, and when. Incomplete information arises from unknown motivations, unknown abilities, or simply differing knowledge of the world. A pure strategy is a complete plan of action; a mixed strategy is a probability distribution over pure strategies; the strategic-form representation lists each firm’s strategy set together with its payoffs. An equilibrium is a profile of strategies in which no firm would unilaterally change its own—crucially, an equilibrium is a fixed point, not the outcome of a dynamic adjustment process, a subtlety that separates equilibrium analysis from the learning dynamics it is sometimes mistaken for.

These equilibrium ideas have a canonical set of applications that recur below: oligopolistic competition in the quantity-setting tradition of Cournot and the price-setting tradition of Bertrand; perfect competition as a limiting case; spatial product competition following Hotelling; entry, with its first-mover advantages and deterrence strategies; and distribution channels. Refinements of the basic Nash concept—subgame perfectness, sequential rationality, and trembling-hand perfectness—discipline which equilibria survive in dynamic and incomplete-information settings, and they matter for substantive questions such as strategic entry deterrence, implicit collusion through price-matching by leader firms, durable-goods pricing by a monopolist, predatory and limit pricing, reputation and product quality, and competitive bidding.

Competition itself does analytical work that bargaining cannot. McAfee and McMillan (1996) shows that competition operates under uncertainty and, in doing so, reveals hidden information: in the independent-private-values benchmark, the selling price in a standard auction equals the second-highest valuation, so the mechanism extracts information that no single negotiation could. Sellers are generally better off revealing what they know, because concealment invites cautious bidding driven by the winner’s curse. Competition is also computationally and strategically cheaper than bargaining—it demands less commitment and less calculation—and it sharpens effort incentives. These themes resurface when we treat auctions, bargaining, and salesforce contests as alternative mechanisms for allocating scarce resources.

31.2 The Craft of Building an Analytical Model

Before deriving any equilibrium it is worth making explicit how an analytical paper is actually constructed, because the logic of discovery differs sharply from the logic of presentation.1 The sequence below distills the practice of theoretical modeling in marketing.

The process begins with a good idea, drawn either from the literature or from industry, and a hard-headed feasibility assessment: is the question interesting, can it be told as a story, who is the target audience, and what is the opportunity cost of pursuing it rather than something else? A counterintuitive piece of advice follows: do not consult the literature too soon. Re-deriving a model that already exists is not wasted effort—it trains the modeler’s judgment, and the act of building independently is what teaches which assumptions matter. The model itself is then built from the simplest possible starting point—one period, two products, a linear consumer utility function—with the formulation written out explicitly, respecting the maxim that everything should be made as simple as possible, but no simpler. Only after the simplest version is solved does one generalize, adding complexity one assumption at a time, so that each new result can be attributed to a specific relaxation. The literature search comes late and serves a sharpening function: finding a related paper invites the productive question of why one did not make the modeling choice the author made. The work concludes with a seminar, where live objection stress-tests the assumptions, and finally with the written paper. Figure 31.1 lays out this workflow as a single sequence, from idea generation through generalization and literature search to the finished paper.

31.3 Spatial Competition: The Hotelling Model

Spatial models are the backbone of analytical marketing because they give product differentiation a geometry. Consumers are arrayed along a line, each firm occupies a location, and the distance between a consumer’s ideal point and a firm’s offering becomes a disutility—literally a transportation cost, figuratively a measure of how poorly the product matches the consumer’s taste. The framework is flexible enough to represent positioning, pricing, advertising, and entry within one consistent geometry, which is why it reappears throughout the chapter.

Hotelling (1929) launched this tradition with a study of stability in competition, arguing—against Bertrand’s critique of Cournot, which Edgeworth had elaborated—that duopoly is inherently unstable, the instability traceable to Cournot’s assumption of absolutely identical products. Consider two sellers, A and B, on a street of length \(l\), located at distances \(a\) and \(b\) from the two ends, with a constant transportation cost \(c\) per unit distance. A consumer located between the firms is indifferent between them when total cost—price plus travel—is equalized. Writing \(x\) and \(y\) for the lengths of the market segments captured to the inside of A and B respectively, the indifferent consumer satisfies

\[ p_1 + cx = p_2 + cy, \tag{31.1}\]

while the segments partition the street,

\[ a + x + y + b = l . \tag{31.2}\]

Solving Equation 31.1 and Equation 31.2 jointly gives the marginal boundaries

\[ x = \tfrac{1}{2}\!\left(l - a - b + \frac{p_2 - p_1}{c}\right), \qquad y = \tfrac{1}{2}\!\left(l - a - b + \frac{p_1 - p_2}{c}\right). \tag{31.3}\]

Each firm’s demand is the length of the street it captures, \(q_1 = a + x\) and \(q_2 = b + y\), so with zero marginal cost the profit functions are

\[ \begin{aligned} \pi_1 = p_1 q_1 &= \tfrac{1}{2}(l + a - b)\,p_1 - \frac{p_1^2}{2c} + \frac{p_1 p_2}{2c},\\ \pi_2 = p_2 q_2 &= \tfrac{1}{2}(l - a + b)\,p_2 - \frac{p_2^2}{2c} + \frac{p_1 p_2}{2c}. \end{aligned} \tag{31.4}\]

The price equilibrium follows from the first-order conditions \(\partial \pi_1/\partial p_1 = 0\) and \(\partial \pi_2/\partial p_2 = 0\), namely

\[ \tfrac{1}{2}(l + a - b) - \frac{p_1}{c} + \frac{p_2}{2c} = 0, \qquad \tfrac{1}{2}(l - a + b) - \frac{p_2}{c} + \frac{p_1}{2c} = 0, \tag{31.5}\]

which solve to the equilibrium prices and quantities

\[ p_1 = c\!\left(l + \frac{a-b}{3}\right),\quad p_2 = c\!\left(l - \frac{a-b}{3}\right),\qquad q_1 = \tfrac{1}{2}\!\left(l + \frac{a-b}{3}\right),\quad q_2 = \tfrac{1}{2}\!\left(l - \frac{a-b}{3}\right), \tag{31.6}\]

with the second-order conditions satisfied. The substantive payoff is a tension between private and social incentives: in the choice of locations, central planning (“socialism”) outperforms decentralized competition (“capitalism”), because firms have a private incentive to cluster that is socially wasteful.

Hotelling (1929) conjectured a Principle of Minimum Differentiation—that firms locate back-to-back at the market center. d’Aspremont, Gabszewicz, and Thisse (1979) demonstrated that the principle is invalid once the price subgame is treated rigorously, because the linear-transport-cost demand is discontinuous: when prices diverge enough that one firm could undercut and seize the entire market, the profit function jumps. Writing the discontinuity explicitly,

\[ \pi_1(p_1, p_2) = \begin{cases} a p_1 + \tfrac{1}{2}(l-a-b)p_1 + \dfrac{p_1 p_2}{2c} - \dfrac{p_1^2}{2c} & \text{if } |p_1 - p_2| \le c(l-a-b),\\[2mm] l\,p_1 & \text{if } p_1 < p_2 - c(l-a-b),\\[1mm] 0 & \text{if } p_1 > p_2 + c(l-a-b), \end{cases} \tag{31.7}\]

and symmetrically

\[ \pi_2(p_1, p_2) = \begin{cases} b p_2 + \tfrac{1}{2}(l-a-b)p_2 + \dfrac{p_1 p_2}{2c} - \dfrac{p_2^2}{2c} & \text{if } |p_1 - p_2| \le c(l-a-b),\\[2mm] l\,p_2 & \text{if } p_2 < p_1 - c(l-a-b),\\[1mm] 0 & \text{if } p_2 > p_1 + c(l-a-b). \end{cases} \tag{31.8}\]

The discontinuity destroys existence of a pure-strategy price equilibrium when firms are close together, so the minimum-differentiation result cannot hold; d’Aspremont, Gabszewicz, and Thisse (1979) restore existence by replacing linear with quadratic transport costs, which yields maximal differentiation instead. The methodological lesson is general: the shape of the transport-cost function is a substantive assumption with first-order consequences, not an innocuous mathematical convenience. KIM and SERFES (2006) later embeds a preference for variety in a location model, foreshadowing the multi-purchase extensions discussed next.

31.4 Positioning Models

Building on the Hotelling skeleton, a stream of work asks where firms locate when the auxiliary assumptions are relaxed. Tabuchi and Thisse (1995) relaxes the assumption that consumers are uniformly distributed. With consumers spread over \([0,1]\) according to a cumulative distribution \(F(x)\) with \(F(1)=1\), two densities are compared: the traditional uniform \(f(x)=1\) and a triangular \(f(x) = 2 - 2|2x - 1|\) that concentrates consumers toward the center. Transportation cost is quadratic in distance. The marginal consumer located between firms at \(x_1 < x_2\) with prices \(p_1, p_2\) is

\[ \bar{x} = \frac{p_2 - p_1 + x_2^2 - x_1^2}{2(x_2 - x_1)}, \tag{31.9}\]

so that profits are \(\Pi_1 = p_1 F(\bar{x})\) and \(\Pi_2 = p_2[1 - F(\bar{x})]\) when \(x_1 < x_2\), with the roles reversed for \(x_1 > x_2\) and a Bertrand subgame when \(x_1 = x_2\). Tabuchi and Thisse (1995) establishes that when firms choose locations simultaneously and then prices simultaneously, and the density is log-concave, a unique Nash price equilibrium exists. Under the uniform density firms locate as far apart as possible—consistent with shopping centers sited away from city centers, though at the cost of forcing consumers to buy products far from their ideal. Under the triangular density no symmetric location equilibrium exists, but two asymmetric equilibria do, with lower profits for both firms. When locations are instead chosen sequentially and prices simultaneously, the first entrant locates at the market center under both densities—a first-mover result that contrasts with the maximal- differentiation outcome of simultaneous choice.

Sajeesh and Raju (2010) turns to variety-seeking, modeling satiation as a relative reduction in willingness to pay for the previously purchased brand—a form of negative state dependence. The received wisdom held that variety-seeking consumers let firms charge higher prices and earn higher profits; Sajeesh and Raju (2010) shows the opposite, that average prices and profits are lower, because firms cut second-period prices to deter switching. The timing is a three-stage game: firms choose locations simultaneously in period 0, prices simultaneously in period 1, and prices again simultaneously in period 2.

Several papers vary the order and structure of competition. K. S. Moorthy (1988) has two identical firms choose product quality first and then price, a two-stage structure we formalize under vertical differentiation in Section 31.11. Tyagi (2000) extends Hotelling (1929), Tyagi (1999b), and Tabuchi and Thisse (1995) to firms that enter sequentially with different cost structures, and—against the usual presumption that moving first is advantageous—demonstrates a second-mover advantage. KIM and SERFES (2006) allows consumers to make multiple purchases, so that some are loyal to a single brand while others consume more than one product, enriching the demand side beyond unit demand. Shreay, Chouinard, and McCluskey (2015) shows that quantity surcharges across different package sizes of the same product—an apparent violation of quantity discounting—can be rationalized by consumer preferences when the sizes are imperfect substitutes, i.e., differentiated products.

31.5 Oligopoly: Market Structure and Frameworks

The spatial models above derive demand from geometry. The oligopoly tradition begins instead from an aggregate demand function and asks how firms compete given it. Three canonical structures organize the field: Bertrand competition, in which firms set prices; Cournot competition, in which firms set quantities; and Stackelberg competition, the leader–follower structure in which one firm commits before the other. Because everything flows from the demand function, it matters where that function comes from; Richard and Martin (1980) derives aggregate demand from primitives rather than positing it, supplying the microfoundation that the reduced-form models take as given. As noted above, K. S. Moorthy (1988) studies how two firms compete on product quality and price under both simultaneous and sequential timing, bridging the spatial and oligopoly traditions.

31.5.1 Cournot Competition: Simultaneous Quantity Setting

Let two firms produce a homogeneous good with constant marginal costs \(c_1, c_2\), so total cost is \(TC_i = c_i q_i\). Inverse demand is linear, \(P(Q) = a - bQ\) with \(Q = q_1 + q_2\). Each firm chooses its quantity to maximize profit,

\[ \pi_1 = [a - b(q_1 + q_2)]q_1 - c_1 q_1, \qquad \pi_2 = [a - b(q_1 + q_2)]q_2 - c_2 q_2 . \tag{31.10}\]

The first-order conditions define each firm’s reaction (best-response) function,

\[ \frac{\partial \pi_1}{\partial q_1} = a - 2 b q_1 - b q_2 - c_1 = 0, \qquad \frac{\partial \pi_2}{\partial q_2} = a - 2 b q_2 - b q_1 - c_2 = 0, \tag{31.11}\]

which rearrange to

\[ q_1 = \frac{a - c_1}{2b} - \frac{q_2}{2} \equiv R_1(q_2), \qquad q_2 = \frac{a - c_2}{2b} - \frac{q_1}{2} \equiv R_2(q_1). \tag{31.12}\]

The Cournot–Nash equilibrium is the intersection of the two reaction functions. Substituting \(R_2\) into \(R_1\) gives \(q_1 = \frac{a-c_1}{2b} - \frac{a-c_2}{4b} + \frac{q_1}{4}\), and solving,

\[ q_1^* = \frac{a - 2c_1 + c_2}{3b}, \qquad q_2^* = \frac{a - 2c_2 + c_1}{3b}, \tag{31.13}\]

with total quantity \(Q = \frac{2a - c_1 - c_2}{3b}\) and equilibrium price \(P = a - bQ = \frac{a + c_1 + c_2}{3}\). The structure is transparent: a firm with lower marginal cost produces more, and the equilibrium price is a simple average of the demand intercept and the two cost levels.

31.5.2 Stackelberg Competition: Sequential Quantity Setting

Now suppose Firm 1 (the leader) chooses quantity in stage 1, and Firm 2 (the follower) responds in stage 2, with common marginal cost \(c_1 = c_2 = c\). Solving by backward induction, the follower’s stage-2 best response is \(R_2(q_1) = \frac{a-c}{2b} - \frac{q_1}{2}\). The leader anticipates this and chooses \(q_1\) to maximize

\[ \pi_1 = \left[a - b\!\left(q_1 + \frac{a-c}{2b} - \frac{q_1}{2}\right)\right] q_1 - c q_1 , \tag{31.14}\]

whose first-order condition \(\frac{a+c}{2} - b q_1 - c = 0\) yields the Stackelberg equilibrium

\[ q_1^* = \frac{a - c}{2b}, \qquad q_2^* = \frac{a - c}{4b}. \tag{31.15}\]

Comparing with the symmetric Cournot outcome \(q_1 = q_2 = \frac{a-c}{3b}\), the leader produces more and the follower less than under simultaneous competition. The leader’s ability to commit first—to move down the follower’s reaction function—is worth real profit, which is the analytical content of “first-mover advantage” in quantity competition. Table 31.2 summarizes the contrast.

| Quantity | Cournot (simultaneous) | Stackelberg (sequential) |

|---|---|---|

| Leader / Firm 1 | \(\dfrac{a-c}{3b}\) | \(\dfrac{a-c}{2b}\) |

| Follower / Firm 2 | \(\dfrac{a-c}{3b}\) | \(\dfrac{a-c}{4b}\) |

| Total \(Q\) | \(\dfrac{2(a-c)}{3b}\) | \(\dfrac{3(a-c)}{4b}\) |

31.5.3 Differentiation and the Value of Independence

When products are differentiated rather than homogeneous, a firm’s profit depends on how substitutable its product is for its rival’s. Let \(\beta\) index substitutability (higher \(\beta\) meaning closer substitutes) and let \(d\) index a second structural parameter such as a demand or cost asymmetry, with \(\bar d\) a threshold. For a “weak” firm \(W\), the comparative static

\[ \frac{d \pi_W^*}{d \beta} < 0 \quad \text{for all } d < \bar{d} \tag{31.16}\]

shows that profit falls as products become closer substitutes, so the weak firm prefers a lower \(\beta\)—it wants a more independent, more differentiated product. For a “strong” firm \(S\), the relationship is non-monotone in \(d\):

\[ \frac{d \pi_S^*}{d \beta} < 0 \quad \text{over a range } d < \bar{d}, \tag{31.17}\]

so that the strong firm’s profit rises as \(\beta\) falls when \(d\) is small, but rises as \(\beta\) increases when \(d\) is large. The substantive reading is that strong firms can benefit from less differentiation (closer substitutes) precisely when the structural asymmetry \(d\) is large, because their strength lets them win the more intense competition that proximity creates—whereas weak firms always seek the shelter of differentiation.

31.6 Entry, Retail Structure, and Conspicuous Consumption

The market-structure machinery extends naturally to questions of entry and the vertical organization of retailing. Dixit (1980) reconsiders the Bain–Sylos postulate, under which an incumbent builds enough capacity to render entry unprofitable. The key insight is one of credibility: investment in capacity deters entry only if it is an irreversible commitment, because if the incumbent can costlessly change capacity after entry, the threat is empty and the incumbent cannot in fact deter entry. Commitment, not capacity per se, is what does the strategic work—a theme shared with the Stackelberg leader’s first-mover commitment.

Tyagi (1999a) decomposes the effect of an additional retailer on prices. The entry of the \((n+1)\)-st retailer sets two forces against each other: a competition effect that lowers retail prices, and an input-cost effect on the wholesale price. Manufacturers, gaining bargaining power as the number of retailers grows, may raise the wholesale price; because each retailer’s quantity choice depends on the wholesale price, this can raise downstream prices, partially or wholly offsetting the competition effect. More retailers therefore need not mean lower consumer prices. Jerath, Sajeesh, and Zhang (2016) reaches a related conclusion through a different channel: when an organized retailer enters a market, inefficient unorganized retailers exit, and the surviving unorganized retailers raise their prices, leaving customers worse off.

Conspicuous consumption introduces consumption externalities into the Hotelling framework. Amaldoss and Jain (2005) models two opposing motives in the pricing of conspicuous goods—a desire for uniqueness and a desire for conformism—and shows they push prices in opposite directions: greater desire for uniqueness raises equilibrium prices and profits, whereas greater desire for conformity lowers them. For a snob who dislikes crowding, utility from the two firms is

\[ U_A = V - p_A - \theta t_s - \lambda_s(n_A), \qquad U_B = V - p_B - (1-\theta) t_s - \lambda_s(n_B), \tag{31.18}\]

while for a conformist who values crowding, the externality enters with the opposite sign,

\[ U_A = V - p_A - \theta t_s + \lambda_c(n_A), \qquad U_B = V - p_B - (1-\theta) t_s + \lambda_c(n_B), \tag{31.19}\]

where \(\theta\) is the consumer’s Hotelling position, \(t_s\) the transport cost, \(\lambda_s\) and \(\lambda_c\) the sensitivities to the externality, and \(n_A, n_B\) the numbers buying each brand. The novel solution concept is rational-expectations equilibrium: the number of buyers a consumer expects must equal the number that in fact materializes. Let \(\theta_s\) mark the marginal snob and \(\theta_c\) the marginal conformist, with \(\beta\) the fraction of snobs in the market. Setting \(U_A = U_B\) for each segment pins down \(\theta_s\) and \(\theta_c\), and the expectations consistency conditions are

\[ \beta \theta_s + (1-\beta)\theta_c = n_A, \qquad \beta(1-\theta_s) + (1-\beta)(1-\theta_c) = n_B, \tag{31.20}\]

where \(\beta \theta_s\) is the mass of snobs buying from A, \((1-\beta)\theta_c\) the mass of conformists buying from A, and the remaining terms the masses buying from B. The equilibrium expectation is realized: what consumers anticipate is what occurs. This expectation is not an empirical expectation in the statistical sense \(\mathbb{E}[\cdot]\)—it carries no measurement error—but an internal-consistency requirement of the model. The striking comparative static, confirmed both analytically and in laboratory tests, is that a price increase can raise snobs’ desire to buy, because higher price enhances the exclusivity the snob values.

Limited editions and exclusivity round out the theme. Balachander and Stock (2009) shows that adding a limited-edition product has a positive direct effect on profits, through the higher willingness to pay it commands, but a negative strategic effect, through the intensified price competition it triggers between brands. Under vertical (quality) differentiation, the high-quality brand gains from limited editions; under horizontal (taste) differentiation, the negative strategic effect lowers equilibrium profits for both brands, yet both still introduce limited editions because not doing so is dominated—a prisoners’-dilemma structure. Sajeesh, Hada, and Raju (2020) distinguishes functionality-oriented from exclusivity-oriented consumer segments and shows that firms increase value enhancements when functionality-oriented consumers perceive greater product differentiation, but decrease them when exclusivity-oriented consumers do, because exclusivity is undercut by enhancements that everyone can enjoy.

31.7 Market Response Models

Optimization of marketing spend requires a function mapping inputs to outputs. The market-response model is that function. Its inputs are marketing instruments— selling effort, advertising spending, promotional spending—and its outputs are sales, share, profit, and awareness. The modeling problem is to choose a functional form flexible enough to capture the empirical regularities of how output responds to input, yet parsimonious enough to estimate and to optimize. Figure 31.2 sets out this input–output logic: controllable marketing actions enter the response function, which maps them to the observed market outcomes.

flowchart LR

subgraph Inputs[Marketing actions: inputs]

A1[Selling effort]

A2[Advertising spend]

A3[Promotional spend]

end

R[(Response<br/>function)]

subgraph Outputs[Observed market outcomes]

O1[Sales]

O2[Share]

O3[Profit]

O4[Awareness]

end

A1 --> R

A2 --> R

A3 --> R

R --> O1

R --> O2

R --> O3

R --> O4

A good dynamic response model captures several stylized facts. Sales response is dynamic, with a growth rate and a decay rate that differ; the steady-state response can be concave or S-shaped, with positive sales even at zero advertising; competitive effects matter; advertising effectiveness itself shifts with media, copy, and other factors; and sales continue to rise or fall even while advertising is held constant. Saunders codified a finer list of phenomena any response form might need to reproduce: zero output at zero input; a linear input–output relationship; decreasing returns to scale; an output ceiling (saturation); increasing returns to scale; an S-shaped pattern in which returns first increase then decrease; a threshold below which input produces no output; and a supersaturation point beyond which additional input reduces output.

31.7.1 A Catalogue of Aggregate Response Forms

No single functional form reproduces every phenomenon, so the modeler chooses among a catalogue, each member of which buys some flexibility at the cost of some. The linear model \(Y = a + bX\) is the simplest but admits only constant returns and so cannot represent concave, convex, or S-shaped response. The power-series / polynomial model \(Y = a + bX + cX^2 + dX^3 + \cdots\) adds curvature but cannot capture saturation or a threshold. The fractional-root / power model \(Y = a + bX^c\) fixes the exponent \(c\) in advance: \(c = \tfrac12\) gives the square-root model, \(c = -1\) the reciprocal model, \(c = 1\) the linear case, \(c < 1\) decreasing returns, \(c > 1\) increasing returns; when \(a = 0\), \(c\) is the constant elasticity. The semilog model \(Y = a + b\ln X\) suits situations in which a constant percentage increase in effort yields a constant absolute increase in sales. The exponential model \(Y = a e^{bX}\) (for \(X > 0\)) gives increasing, convex returns when \(b > 0\) and decreasing returns with saturation when \(b < 0\). The modified exponential \(Y = a(1 - e^{-bX}) + c\) delivers decreasing returns and saturation, with upper bound \(a + c\) and lower bound \(c\), and is the workhorse for selling-effort response. The logistic \(Y = \frac{a}{a + e^{-(b + cX)}} + d\) produces increasing-then-decreasing returns—an S-shape—with saturation at \(a + d\), and is preferred when both saturation and an S-shape are required; the Gompertz model is a related asymmetric S-curve.

The ADBUDG model of Little (1970),

\[ Y = b + (a - b)\frac{X^c}{d + X^c}, \tag{31.21}\]

is the most versatile of the single-instrument forms: it is S-shaped when \(c > 1\) and concave with a saturation effect when \(0 < c < 1\), with upper bound \(a\) and lower bound \(b\). It passes through the origin or not as specified, handles concavity, saturation, and S-shapes within one expression, and is standard for advertising and selling-effort response. Multiple instruments are accommodated additively, \(Y = a f(X_1) + b g(X_2)\); multiplicatively, \(Y = a X_1^b X_2^c\) with \(b\) and \(c\) as elasticities, or more generally \(Y = a f(X_1)\cdot b g(X_2)\); or in a combined multiplicative-and-additive form \(Y = a f(X_1) + b g(X_2) + c f(X_1) g(X_2)\) that allows interaction between instruments. Finally, the dynamic response model \(Y_t = a_0 + a_1 X_t + \lambda Y_{t-1}\) separates the current effect \(a_1\) from the carry-over effect \(\lambda\), the lagged influence of past sales on present sales.

31.7.2 Dynamic Effects and Adstock

Marketing effects rarely land all at once. The carry-over effect captures how current expenditure influences future sales—advertising adstock is precisely this lagged effect of advertising on sales. Related dynamics include the delayed-response effect (a lag between investment and impact), customer-holdout effects, hysteresis (persistent effects that do not reverse when spend reverses), new-trier and wear-out effects, and stocking effects whereby promotions shift purchase timing. The simplest decay model writes adstock as a geometrically weighted sum of current and lagged spend,

\[ A_t = T_t + \lambda T_{t-1}, \qquad t = 1, 2, \dots, \tag{31.22}\]

where \(A_t\) is adstock at time \(t\), \(T_t\) is advertising spend at \(t\), and \(\lambda\) is the decay (lag-weight) parameter governing how slowly past advertising depreciates.

Response models can be classified along six axes that, together, determine which form is appropriate: the number of marketing variables; whether competition is included; the nature of the input–output relationship (linear versus S-shaped); whether the setting is static or dynamic; whether response is individual or aggregate; and the level of demand analyzed (sales versus market share).

31.7.3 From Category Sales to Brand Share

Brand sales factor into category demand and within-category share, \(Y = M \times V\), where \(Y\) is brand sales, \(V\) is product-class (category) sales, and \(M\) is market share. The dominant family for the share component is the attraction model, in which a brand’s share equals its attractiveness relative to the total attractiveness in the category,

\[ M_i = \frac{A_i}{A_1 + \cdots + A_n}, \tag{31.23}\]

with \(A_i\) the attractiveness of brand \(i\). Attraction models guarantee shares that are non-negative and sum to one—a logical-consistency property that ad hoc share regressions lack.

At the individual level, the multinomial logit model gives the probability that consumer \(i\) chooses brand \(l\) as

\[ P_{il} = \frac{e^{A_{il}}}{\sum_j e^{A_{ij}}}, \tag{31.24}\]

where \(A_{ij} = \sum_k w_k b_{ijk}\) is the attractiveness of product \(j\) to consumer \(i\), \(b_{ijk}\) is consumer \(i\)’s evaluation of product \(j\) on attribute \(k\), the sum running over the products \(i\) considers, and \(w_k\) is the importance weight on attribute \(k\). The logit is the individual-level microfoundation of the aggregate attraction model and the bridge to the choice-modeling tradition of Guadagni and Little (1983); we treat its estimation in the conjoint and choice-modeling discussion below.

31.7.4 Worked Illustration: Estimating an ADBUDG Response Curve

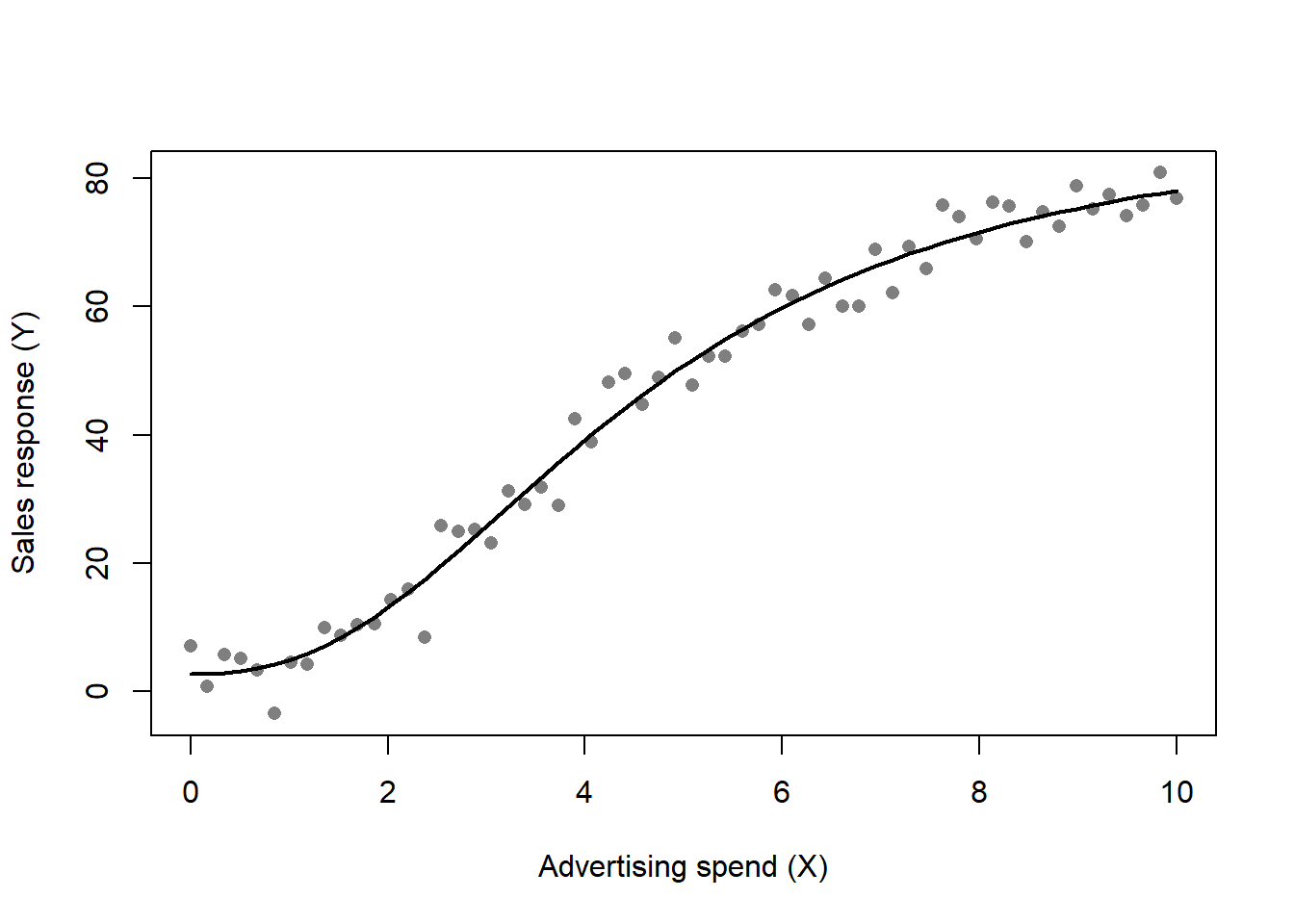

To make the response-modeling apparatus concrete, the following code simulates an advertising response that is genuinely S-shaped, then recovers the ADBUDG parameters by nonlinear least squares and plots the fit, shown in Figure 31.3. The example is seeded for reproducibility.

Code

set.seed(2026)

# True ADBUDG parameters: Y = b + (a - b) * X^c / (d + X^c)

a_true <- 100 # upper bound (saturation)

b_true <- 5 # lower bound (sales at zero advertising)

c_true <- 2.2 # S-shape (c > 1)

d_true <- 40

adbudg <- function(X, a, b, c, d) b + (a - b) * X^c / (d + X^c)

X <- seq(0, 10, length.out = 60)

Y_mean <- adbudg(X, a_true, b_true, c_true, d_true)

Y <- Y_mean + rnorm(length(X), sd = 4)

fit <- nls(

Y ~ b + (a - b) * X^c / (d + X^c),

start = list(a = 90, b = 10, c = 1.5, d = 30)

)

round(coef(fit), 2)

#> a b c d

#> 89.38 2.71 2.42 39.16

plot(X, Y, pch = 16, col = "grey50",

xlab = "Advertising spend (X)", ylab = "Sales response (Y)")

lines(X, predict(fit, newdata = list(X = X)), lwd = 2)

31.8 Conjoint and Augmented Conjoint Analysis

Conjoint analysis estimates how consumers trade off product attributes, and the analytical-modeling literature has extended it from preference measurement toward managerially decisive quantities such as reservation prices. The core of conjoint is treated in Section 37.2; here the concern is the augmentations that connect attribute part-worths to pricing and demand.

Jedidi and Zhang (2002) augments conjoint to estimate consumer reservation prices—the maximum a consumer would pay—rather than mere preference rankings. Starting from a rating-based utility specification

\[ \text{Utility (rating)} = \alpha + \sum_i \beta_i\, \text{Attribute}_i, \tag{31.25}\]

with \(\alpha\) a baseline constant and \(\beta_i\) the part-worth of attribute \(i\), the method maps estimated part-worths into reservation prices for a product in a category. The resulting estimates support decisions about product introduction, the switching effect (consumers drawn from rival brands), the cannibalization effect (consumers drawn from the firm’s own existing products), and the market-expansion effect (new demand created). Netzer and Srinivasan (2011) decomposes conjoint into a sequence of constant-sum paired-comparison questions, which not only estimates attribute importances but also yields standard errors for each importance weight—a statistical refinement that lets the analyst distinguish attributes that genuinely matter from those whose apparent importance is noise.

31.9 Distribution Channels

A channel is a vertical sequence of firms—manufacturers upstream, retailers downstream—each setting prices or quantities to maximize its own profit. The central analytical phenomenon is double marginalization: when an upstream firm marks up over cost and a downstream firm marks up again over the wholesale price, the final price exceeds the integrated-monopoly price and channel profit falls. Whether to integrate, and how to coordinate, are the questions the channel literature answers.

McGuire and Staelin (1983) is the foundational treatment. Two manufacturers produce differentiated, competing products and reach consumers through downstream retailers. Three vertical structures are compared: a decentralized system with two manufacturers and two independent retailers (four players); a vertically integrated system in which each manufacturer owns its retailing (two players); and a mixed system with one integrated manufacturer and one manufacturer–independent-retailer pair (three players). Each retail outlet faces a downward-sloping demand \(q_i = f_i(p_1, p_2)\); under the decentralized system the Nash-equilibrium retail demands become functions of the wholesale prices, \(q_i^* = g_i(w_1, w_2)\). The decision variables are prices, not quantities, and retail demand is assumed linear in prices. Figure 31.4 contrasts the three vertical structures, from the fully decentralized four-player system to the fully integrated two-player one.

flowchart TD

subgraph Dec[Decentralized: 4 players]

M1[Mfr 1] --> R1[Retailer 1]

M2[Mfr 2] --> R2[Retailer 2]

end

subgraph Mix[Mixed: 3 players]

M3[Mfr 1] --> R3[Retailer 1]

M4[Mfr 2 integrated store]

end

subgraph Int[Integrated: 2 players]

M5[Mfr 1 integrated store]

M6[Mfr 2 integrated store]

end

The demand system, after specifying linear retail demands, is

\[ q_1' = \mu S\!\left[1 - \frac{\beta}{1-\theta}\,p_1' + \frac{\beta\theta}{1-\theta}\,p_2'\right], \tag{31.26}\]

\[ q_2' = (1-\mu) S\!\left[1 + \frac{\beta\theta}{1-\theta}\,p_1' - \frac{\beta}{1-\theta}\,p_2'\right], \tag{31.27}\]

with \(0 \le \mu, \theta \le 1\) and \(\beta, S > 0\). Here \(S\) is a scale factor equal to industry demand \(q' \equiv q_1' + q_2'\) at zero prices, \(\mu\) governs the asymmetry in demand between firms, and \(\theta\) measures substitutability—the ratio of the cross-price sensitivity to the own-price sensitivity. At \(\theta = 0\) demands are independent and each firm is a monopolist; as \(\theta \to 1\) the products become maximally substitutable. Feasibility requires that prices cover fixed manufacturing and selling costs \(m'\) and \(s'\) and that demands stay non-negative,

\[ P = \{\, p_1', p_2' \mid p_i' - m' - s' \ge 0,\ i=1,2;\ (1-\theta) - \beta p_1' + \beta\theta p_2' \ge 0,\ (1-\theta) + \beta\theta p_1' - \beta p_2' \ge 0 \,\}, \tag{31.28}\]

which forces \(\beta \le \frac{1}{m' + s'}\); and for industry demand not to rise with either price, \(\frac{\theta}{1+\theta} \le \mu \le \frac{1}{1+\theta}\). After rescaling, industry demand is \(q = 2(1-\theta)(p_1 + p_2)\).

The central result connects channel design to substitutability. When each manufacturer is a monopolist (\(\theta = 0\)), selling through a private (independent) channel is twice as profitable as integrating. When demand is maximally driven by rival retailers’ actions (\(\theta \to 1\)), private dealers are three times as profitable. The break-even degree of substitutability is \(\theta \approx 0.708\). The conclusion is that the optimal distribution system depends on the degree of substitutability at the retail level: decentralization, by softening downstream price competition, can be a strategic asset rather than merely a source of double marginalization.

A complementary literature studies channel coordination devices. Jeuland and Shugan (2008) catalogues four rationales for quantity discounts—cost-based economies of scale, demand-based reasons (large buyers are more price-sensitive), strategic single-sourcing, and channel coordination—and contributes the last, showing how a quantity-discount schedule can align an independent retailer’s incentives with the manufacturer’s. K. S. Moorthy (1987) analyzes second-degree price discrimination as a channel and screening device, while Geylani, Dukes, and Srinivasan (2007) and Jerath and Zhang (2010) extend the channel framework to the strategic interaction between powerful retailers and manufacturers.

31.10 Advertising Models

Advertising enters consumer utility through three distinct mechanisms, and the choice among them is the central modeling decision. Informative advertising increases overall demand for the brand by informing more consumers of its existence; persuasive advertising shifts demand toward the brand by raising perceived value or loyalty; comparative advertising shifts demand away from a competitor. The spatial Hotelling framework hosts all three cleanly. With \(n\) consumers distributed uniformly along the line—an apt assumption for a mature market with stable demand—base utilities are

\[ U_A = V - p_A - t x, \qquad U_B = V - p_B - t(1-x), \tag{31.29}\]

where \(t\) is the transport cost, reinterpretable here as a return-on-advertising parameter.

Persuasive advertising can be modeled as scaling the value term, \(U_A = A_A V - p_A - tx\), or as raising the reservation price through a concave transformation, \(U_A = \sqrt{Ad_A}\,V - p_A - tx\), or as effectively pulling the firm’s product closer to the consumer’s ideal, \(U_A = V - p_A - \frac{tx}{\sqrt{Ad_A}}\). Comparative advertising instead inflates the rival’s effective distance,

\[ U_A = V - p_A - t\sqrt{Ad_B}\,x, \qquad U_B = V - p_B - t\sqrt{Ad_A}\,(1-x). \tag{31.30}\]

The marginal consumer solves \(U_A = U_B\), giving

\[ x = \frac{1}{t\sqrt{Ad_A} + t\sqrt{Ad_B}}\left(-p_A + p_B + t\sqrt{Ad_A}\right), \tag{31.31}\]

so the (concave) profit functions, net of advertising cost, are

\[ \pi_A = p_A\, x\, n - \phi\, Ad_A, \qquad \pi_B = p_B (1-x)\, n - \phi\, Ad_B, \tag{31.32}\]

with \(\phi\) the per-unit cost of advertising (higher for television than for online, say) and \(t\) interpreted as the return on advertising. Solving the price subgame conditional on advertising levels yields

\[ p_A = \tfrac{2}{3} t\sqrt{Ad_A} + \tfrac{1}{3} t\sqrt{Ad_B}, \qquad p_B = \tfrac{1}{3} t\sqrt{Ad_A} + \tfrac{2}{3} t\sqrt{Ad_B}. \tag{31.33}\]

Prices rise with advertising intensity—invest more, charge more—and each firm’s price rises in its rival’s advertising as well. Optimizing advertising given these prices, the symmetric competitive equilibrium is

\[ Ad_A = Ad_B = \frac{25\, t^2 n^2}{576\, \phi^2}, \qquad p_A = p_B = \frac{5\, t^2 n}{24\, \phi}. \tag{31.34}\]

As the cost of advertising \(\phi\) rises, firms advertise less; as the return \(t\) rises, they benefit more. Notably, equilibrium prices are higher with advertising than without it. Because colluding on prices is illegal and easily detected while colluding on advertising is hard to observe, firms may tacitly coordinate on advertising—pulsing, for instance.2 Setting a common collusive level \(Ad_A = Ad_B = Ad\),

\[ Ad_A = Ad_B = \frac{t^2 n^2}{16\, \phi^2} > \frac{25\, t^2 n^2}{576\, \phi^2}, \tag{31.35}\]

the collusive advertising level exceeds the competitive one, supporting higher prices and leaving consumers worse off. A model combining comparative and persuasive advertising writes the rival’s relative advertising into the transport term,

\[ U_A = V - p_A - tx\,\frac{\sqrt{Ad_B}}{\sqrt{Ad_A}}, \qquad U_B = V - p_B - t(1-x)\,\frac{\sqrt{Ad_A}}{\sqrt{Ad_B}} . \tag{31.36}\]

Informative advertising, by contrast, works by increasing the number \(n\) of potential customers—the natural specification for a new product whose pool of aware consumers is still growing. A subtle assumption throughout is that the advertising decision precedes the pricing decision, which is reasonable because prices are easy to adjust while advertising budgets are committed at the start of a period. Consumption itself responds to availability: consumers consume more when stock is plentiful and less when it is scarce (Ailawadi and Neslin 1998).

The empirical and theoretical literature refines these mechanisms. Villas-Boas (1993) shows that under monopoly, firms do better to pulse—alternating between a minimum and an efficient level of advertising—because the advertising response function is S-shaped; the analysis assumes Markov strategies, so that current actions depend only on payoff-relevant state rather than on history, and establishes that if the loss from letting the consideration level lapse exceeds the efficient advertising expenditure, the unique Markov-perfect equilibrium has both firms always advertising.

Nelson (1974) supplies the information-economics foundation that distinguishes advertising by what consumers can verify. Search qualities are knowable before purchase; experience qualities are not. Misleading advertising risks credibility and imposes the cost of processing non-buying customers, and there is an inverse association between quality produced and utility-adjusted price. Firms that wish to sell more advertise more, and they advertise to their natural audience—those whose tastes a brand best serves are the most likely to see its advertisement. Advertising for experience qualities conveys information indirectly (chiefly by signaling that the seller finds it worthwhile to advertise), whereas advertising for search qualities conveys it directly. Goods are accordingly classified by whether their quality variation is search- or experience-based, into experience durables, experience nondurables, and search goods. Experience goods are advertised more, because advertising raises sales by raising the seller’s reputability; the marginal revenue of advertising is nonetheless higher for search goods, which concentrate in newspapers and magazines while experience goods migrate to other media. For experience goods, word of mouth is a better information source than advertising, and purchase frequency moderates the contrast—low- frequency purchases lean on word of mouth. When laws against deception are moderately enforced, deceptive advertising flourishes: too little enforcement and consumers distrust all claims, too much and deception is deterred, but a moderate regime lets consumers believe and advertisers cheat, which is why experience goods—where enforcement concentrates—carry more deceptive advertising.

Targeting sharpens these effects. Iyer, Soberman, and Villas-Boas (2005) shows that firms advertising to their targeted market—consumers with a strong preference for their product—rather than to competitors’ loyalists endogenously increase market differentiation and raise equilibrium profits. Targeted advertising is more valuable than targeted pricing: targeted advertising raises profits whether or not firms also price-discriminate, whereas targeted pricing merely intensifies competition for comparison shoppers without improving equilibrium profits. The mass of comparison shoppers is \(s = 1 - 2h\), where \(h\) is the size of each firm’s loyal segment and thus also indexes the differentiation between firms; \(A\) denotes the cost of advertising to the entire market and \(r\) the reservation price. Chen et al. (2009) distinguishes combative from constructive advertising and integrates the informative, complementary, and persuasive mechanisms: informative advertising raises awareness, lowers search costs, and increases differentiation; complementary advertising raises utility by signaling social prestige; persuasive advertising lowers price sensitivity, with combative advertising a special case. Consumer response moderates the effect of combative advertising on price competition—it generally decreases competition, but it increases competition when consumer preferences are biased toward advertising firms and disfavored firms cannot advertise and can only respond on price, because an advertising war then spills into a price war.

31.11 Product Differentiation, Quality, and Asymmetric Information

Differentiation comes in two forms with very different welfare logic. Horizontal differentiation means different consumers prefer different products—there is no universal ranking—and is naturally represented by a quadratic taste loss,

\[ U = V - p - t(\theta - a)^2, \tag{31.37}\]

where \(\theta\) is the consumer’s ideal point and \(a\) the product’s location. Vertical differentiation means one product is unambiguously better: all consumers agree on the ranking and differ only in willingness to pay for quality. With qualities \(s_A, s_B\) and a taste parameter \(\theta\),

\[ U_A = \theta s_A - p_A, \qquad U_B = \theta s_B - p_B, \tag{31.38}\]

where \(\theta\) is the consumer’s position on the quality-valuation line and a consumer buys only if utility is non-negative. Taking \(B\) as the higher-quality product, the consumer indifferent between the two is found from \(\theta s_B - p_B = \theta s_A - p_A\), giving the boundary

\[ \bar{\theta} = \frac{p_B - p_A}{s_B - s_A}. \tag{31.39}\]

At equal prices every consumer prefers the higher quality, the characteristics approach treating a product as the bundle of its characteristics.

K. S. Moorthy (1988) closes the vertical-differentiation model with quality-dependent costs. With profits \(\pi_A = (p_A - c s_A^2)\,\text{(share}_A)\) and \(\pi_B = (p_B - c s_B^2)\, \text{(share}_B)\) and the lower boundary \(\bar\theta_2 = p_A / s_A\) marking the consumer indifferent between buying the low-quality product and not buying, the two firms choose qualities first and prices second, and differentiate their qualities to relax price competition. Wauthy (1996) characterizes when the market is covered: with \(\theta\) drawn over a support of width \(b/a\), full coverage requires

\[ 2 \le \frac{b}{a} \le \frac{2 s_2 + s_1}{s_2 - s_1}. \tag{31.40}\]

A modeling subtlety follows: with \(\theta \in [0,1]\) one cannot simultaneously have full market coverage, so the support is often re-specified, for instance

\[ \theta \in \begin{cases} [1,4] & \text{if } b/a = 4,\\ [1,2] & \text{if } b/a = 2, \end{cases} \tag{31.41}\]

to obtain coverage while preserving the vertical structure.

31.11.1 Asymmetric Information: Adverse Selection and Signaling

Quality is often unobservable at the point of purchase, and the consequences are profound. Two failures must be distinguished by their timing relative to the contract. Adverse selection is a pre-contract problem: a relevant characteristic is uncertain before agreement. Moral hazard is a post-contract problem: intentions or actions are hidden after agreement. The adverse-selection problem can unravel a market entirely.

A transparent setup adapts Akerlof’s used-car market. Car quality is \(\theta \in [0,1]\); a seller owning a car of type \(\theta\) values it at \(\theta\), while a buyer’s willingness to pay is \(\tfrac{3}{2}\theta\), so trade is mutually beneficial whenever it occurs. If quality is observable to both sides, any price \(p(\theta) \in [\theta, \tfrac{3}{2} \theta]\) supports trade and both parties gain. If quality is unobservable but symmetrically so—neither side knows \(\theta\), which is uniform—then \(\mathbb{E}[\theta] = \tfrac12\), the seller’s expected value is \(\tfrac12\), the buyer’s is \(\tfrac{3}{2}\cdot \tfrac12 = \tfrac34\), and trade occurs at any \(p \in [\tfrac12, \tfrac34]\). But under genuine asymmetric information—only the seller knows \(\theta\)—a seller offers a car only if \(p \ge \theta\), so the cars on offer have quality in \([0, p]\), and a buyer reasoning correctly computes \(\mathbb{E}[\theta \mid \theta \le p] = \tfrac12 p\), giving buyer utility \(\tfrac34 p < p\). The buyer’s value falls short of the price for every \(p\), and no trade occurs. Asymmetric information, not uncertainty per se, is what destroys the market.

Akerlof (1970) is the founding analysis of this adverse-selection mechanism, framed as the relationship between quality and uncertainty in the automobile market across a \(2\times 2\) of used-versus-new and good-versus-bad. Let \(q\) be the probability of a good car and \(1-q\) the probability of a lemon. Sellers know the probability that a given car is bad; buyers do not, and pay the same price for a lemon as for a good car. The result contrasts with Gresham’s law: bad money drives out good only because the exchange rate is fixed and the two are distinguishable, whereas the buyer cannot tell a good car from a lemon at all. Formally, demand depends on price and average quality, \(Q^d = D(p, \mu)\); supply depends on price, \(S = S(p)\); and average quality is itself a function of price, \(\mu = \mu(p)\), with equilibrium \(S(p) = D(p, \mu(p))\)—and the punchline is that at no price will any trade happen.

Akerlof (1970) makes this concrete with two trader groups. The first has utility \(U_1 = M + \sum_{i=1}^n x_i\) and the second \(U_2 = M + \sum_{i=1}^n \tfrac{3}{2} x_i\), where \(M\) is consumption of other goods, \(x_i\) is the quality of car \(i\), and \(n\) the number of cars, with incomes \(Y_1, Y_2\). Group-1 demand is

\[ D_1 = \begin{cases} Y_1 / p & \text{if } \mu/p > 1,\\ 0 & \text{if } \mu/p < 1, \end{cases} \tag{31.42}\]

and with quality uniform, the supply offered by group 1 is \(S_1 = pN/2\) for \(p \le 2\), carrying average quality \(\mu = p/2\). Group-2 demand is

\[ D_2 = \begin{cases} Y_2 / p & \text{if } \tfrac{3}{2}\mu > p,\\ 0 & \text{if } \tfrac{3}{2}\mu < p, \end{cases} \tag{31.43}\]

with \(S_2 = 0\). Total demand under asymmetric information is therefore

\[ D(p, \mu) = \begin{cases} (Y_1 + Y_2)/p & \text{if } p < \mu,\\ Y_2 / p & \text{if } \mu < p < \tfrac{3}{2}\mu,\\ 0 & \text{if } p > \tfrac{3}{2}\mu, \end{cases} \tag{31.44}\]

and since average quality at price \(p\) is \(\mu = p/2\), the middle and upper branches bind and no trade occurs. Under symmetric information the market revives: with quality uniform on \([0,2]\), supply is \(S(p) = N\) for \(p > 1\) and zero otherwise, demand is \((Y_1+Y_2)/p\) for \(p<1\), \(Y_2/p\) for \(1<p<\tfrac32\), and zero above, and equilibrium price is

\[ p = \begin{cases} 1 & \text{if } Y_2 < N,\\ Y_2 / N & \text{if } \tfrac{2}{3}Y_2 < N < Y_2,\\ \tfrac{3}{2} & \text{if } N < \tfrac{2}{3}Y_2, \end{cases} \tag{31.45}\]

so trade resumes once quality is commonly observed. The mechanism generalizes to insurance for the elderly, the employment of minorities, the cost of dishonesty, and credit markets in developing economies, and the institutional remedies—guarantees, brand names, retail chains, and licensing—are precisely the devices that re-establish trust where quality is uncertain.

Spence (1973) builds the signaling response to adverse selection on Akerlof’s foundation. Two worker types produce one and two units respectively, with a fraction \(\alpha\) of type 1 and \(1-\alpha\) of type 2, so average productivity is \(\mathbb{E}[P] = \alpha + 2(1- \alpha) = 2 - \alpha\). Workers can signal type through education, whose cost is \(E\) for type 1 and \(E/2\) for the more able type 2. A separating equilibrium requires the signal to be incentive-compatible: type 1 must find it not worthwhile to acquire the education, \(2 - E < 1 \Rightarrow E > 1\), while type 2 must find it worthwhile, \(2 - E/2 > 1 \Rightarrow E < 2\). Any cost \(1 < E < 2\) therefore sustains a separating equilibrium in which education credibly distinguishes the types even though it adds nothing to productivity—the canonical demonstration that a costly, otherwise-useless signal can convey information when its cost is differentially borne.

S. Moorthy and Srinivasan (1995) carries the signaling logic into marketing through money-back guarantees. A guarantee signals quality, the transaction cost being whatever the buyer or seller pays to redeem it; the guarantee refunds the purchase price without compensating the buyer’s own return expense. If signaling were costless, money-back guarantees and price would be interchangeable signals. Because signaling is costly, the results sharpen: with homogeneous buyers, a low-quality seller cannot profitably mimic a high-quality seller’s guarantee. With heterogeneous buyers, the picture is richer—when transaction costs are very high the seller forgoes the guarantee or signals through price instead, and when they are moderate there is a critical value of seller transaction cost below which the high-quality seller’s profit increases in transaction cost and above which it decreases. A striking corollary is that uninformative advertising—“money-burning” expenditure that does not shift demand directly—is never needed when a guarantee is available. Moral hazard remains a caveat: consumers may exhaust the product’s value within the guarantee window before claiming a refund. Table 31.3 lays out the seller’s cost structure, the engine of the separating equilibrium.

| High-quality seller (\(h\)) | Low-quality seller (\(l\)) | |

|---|---|---|

| Unit cost (\(c_h > c_l\)) | \(c_h\) | \(c_l\) |

31.12 Bargaining

Bargaining is the allocation mechanism for the thinnest of markets: one buyer and one seller. Table 31.4 places it among the alternatives—many buyers and many sellers constitute a traditional market, many buyers and one seller an auction, and one buyer and one seller a bargaining problem. Before invoking game theory at all, a share may be fixed by an arbitrator, by meeting in the middle, or by a forced-final take-it-or-leave-it move. Negotiation is the art; bargaining is the science; game theory’s contribution is to the rules of the encounter, and the area remains fertile for research.

| Buyers and sellers | Allocation type |

|---|---|

| Many buyers and many sellers | Traditional market |

| Many buyers and one seller | Auction |

| One buyer and one seller | Bargaining |

31.12.1 Non-cooperative Bargaining

The non-cooperative approach specifies the rules explicitly and solves for the subgame-perfect outcome. The simplest rule is a take-it-or-leave-it offer over a cake: if the responder accepts, the parties trade; if she rejects, no one eats. Under perfect information this has a trivial rollback equilibrium. More realistically, bargaining is “take-it-or-counteroffer,” and time has value: both parties prefer to trade sooner, so delay—labor negotiations dragging into strikes and work stoppages—destroys surplus.

Consider two-stage bargaining over a cake. In the first period I offer you a share, keeping proportion \(p\); if you reject, you counteroffer, but a fraction \(\delta\) of the cake melts in the interim. Payoffs are \((1-p, p)\) if you accept immediately and \(\big((1-\delta)(1-p),\,(1-\delta)p\big)\) in the second period. Because period 2 is the final period, it is itself a take-it-or-leave-it offer: you will offer me the smallest slice I will accept, keeping essentially all of the remaining \(1-\delta\). Rolling back, in period 1 I must give you at least the surplus you would secure by waiting. Your second-period surplus is \(1-\delta\), so you accept a first-period offer only if your share \(p \ge 1 - \delta\); I therefore offer you exactly \(1-\delta\) and we settle immediately. The comparative static is sharp: the more patient you are—the slower the cake melts, the smaller is \(\delta\)—the more you receive now. Whether the first or second mover is advantaged depends on \(\delta\): a fast-melting cake (high \(\delta\)) favors the first mover, a slow-melting one (low \(\delta\)) the second. Either way, if both parties reason, agreement is reached in the first period, and the general lesson is to strike a deal as early as possible.

Why, then, do real negotiations delay? Reputation-building and a lack of information. Information asymmetry is the deeper answer—uncertainty about the likelihood of success, as in civil litigation. Each side has a reservation price (in a lawsuit, its expectation of winning) that is unknown to the other; one must probabilistically choose a best offer, accepting that the very probability implies a chance that no bargain is struck. The rules of the game uniquely determine the outcome; which rules favor whom depends on patience and information; and persistent delay means someone must be wrong.

A worked screening example shows information at work. A company negotiates with a union. The firm is “highly profitable” (annual profit $200k) with probability \(p\); a strike costs the firm 10% of annual profits. If the union demands a $150k wage it is surely accepted; if it demands $200k it is accepted only with probability \(p\), for an expected wage of \(200p\). At \(p = 0.9\) the best opening demand is $200k, worth \(0.9 \times 200 = 180\); at \(p = 0.1\) a $200k demand is worth only \(0.1 \times 200 = 20\), so the union does better to ask $150k—it is not worth the risk. Now suppose a first-period offer can be rejected at the cost of a strike. Because a strike costs a high-profit firm more than a low-profit firm, the union can use time to screen. If the union asks $170k in period 1, a low-profit firm (worth $150k) rejects because it cannot afford to accept, while a high-profit firm weighs rejection—at best the union strikes and then asks only $140k, but the strike has meanwhile cost the firm $20k—and accepts. The result is a separating equilibrium: only high-profit firms accept in the first period, and a rejection reveals a low-profit firm, against which the union then asks $140k. The union’s apparent “giving in” after a rejection is not weakness but screening—different firm types value the future differently, and time is the screening device.

31.12.2 Cooperative Bargaining and the Nash Solution

The cooperative approach abstracts from the procedural rules and asks what division should result, given axioms the solution must satisfy. Two people divide a sum: if they disagree each gets nothing, and they cannot divide more than the whole. Nash (1950) founds the axiomatic theory for this bilateral-monopoly, nonzero-sum two-person game, in which no action by one party, without the other’s consent, can affect the other’s gain. The assumptions are rational individuals who maximize gain, full knowledge of tastes and preferences, transitive ordering (\(A \succ C\) whenever \(A \succ B\) and \(B \succ C\)), and continuity. Utility is ordinal-plus: \(u(A) > u(B)\) means \(A\) is preferred, and the linearity property requires that for \(0 \le p \le 1\), \(u(pA + (1-p)B) = p\,u(A) + (1-p)\,u(B)\), extending to two persons as \(p[A,B] + (1-p)[C,D] = [pA + (1-p)C,\ pB + (1-p)D]\). An anticipation \(pA + (1-p)B\) is a lottery giving event \(A\) with probability \(p\).

Let \(u_1, u_2\) be the players’ utility functions and \(c(S)\) the solution point selected from a bargaining set \(S\) that is compact, convex, and contains the disagreement point at the origin. Nash (1950) characterizes \(c(S)\) by three axioms. Efficiency: if some \(\beta \in S\) gives both players strictly more than \(\alpha \in S\), then \(\alpha \neq c(S)\)—players maximize utility. Independence of irrelevant alternatives: if \(S \subseteq T\) and \(c(T) \in S\), then \(c(T) = c(S)\). Symmetry: if \(S\) is symmetric about the line \(u_1 = u_2\), then \(c(S)\) lies on that line, encoding equal bargaining power. These axioms uniquely select the division that maximizes the product of the players’ gains over their disagreement payoffs—the Nash bargaining solution.

The bargaining lens illuminates channel power. Iyer and Villas-Boas (2003) shows that the presence of a powerful retailer such as Walmart can benefit all channel members, not merely the retailer, by reshaping the terms of trade. Desai and Purohit (2004) analyzes haggling: with two consumer segments—hagglers and non-hagglers—a haggling policy can be more profitable than fixed pricing when the proportion of non-hagglers is sufficiently high, because the firm extracts surplus from hagglers without sacrificing the non-hagglers who pay the posted price.

31.13 Pricing and Search Theory

If all consumers were perfectly informed, the law of one price would hold and price dispersion would be a puzzle. Search theory resolves the puzzle by recognizing that information is costly, and that the resulting mix of informed and uninformed consumers can sustain dispersion as an equilibrium phenomenon rather than a disequilibrium artifact.

Varian and Purohit (1980) builds an equilibrium theory of price dispersion on the foundation laid by Stigler and developed by Salop and Stiglitz (1977) and Stiglitz and Salop (1982). Dispersion comes in two flavors: spatial dispersion, arising when uninformed and informed consumers coexist—though it need not persist, since consumers learn from experience over time—and temporal dispersion, manifest as sales. Varian and Purohit (1980) follows Stiglitz and Salop (1982), who assumes informed consumers who buy at the lowest-price store and uninformed consumers who choose a store at random, and Shilony (1977), who studies randomized pricing strategies. Let \(I > 0\) be the number of informed consumers, \(M > 0\) the number of uninformed, and \(n\) the number of stores, so \(U = M/n\) uninformed consumers patronize each store. Each store draws its price from a density \(f(p)\): it succeeds—charging the lowest of the \(n\) prices—and then serves \(I + U\) customers, or it fails and serves only \(U\); stores tying at the lowest price split the informed segment equally. With cost curve \(c(q)\), the price \(p^* = c(I+U)/(I+U)\) is the average cost at the maximal customer count. Varian and Purohit (1980) establishes a sequence of properties of the equilibrium mixed strategy: the density vanishes outside \([p^*, r]\) where \(r\) is the reservation price (Prop. 1); no symmetric pure-price equilibrium exists (Prop. 2); the equilibrium has no point masses (Prop. 3); where \(f(p) > 0\), the indifference condition

\[ \pi_s(p)\,(1 - F(p))^{n-1} + \pi_f(p)\,\big[1 - (1 - F(p))^{n-1}\big] = 0 \tag{31.46}\]

holds, equating the expected profit from a successful and a failed price draw (Prop. 4); the quantity \(\pi_f(p)\,(\pi_f(p) - \pi_s(p))\) is strictly decreasing in \(p\) (Prop. 5); the distribution puts positive mass just above \(p^*\) and below \(r\) (Props. 6–7); and there are no gaps in the support (Prop. 8). Whether a consumer chooses to become informed is itself endogenous, turning on the “full price” of search—search costs plus any fixed cost of information.

Lazear (1984) turns to retail pricing and clearance sales, asking how a good’s characteristics, the thinness of its market, and its time on the shelf shape its price path. In a single-period model, let \(V\) be the valuation of the lone potential buyer, with prior density \(f(V)\) and distribution \(F(V)\); the firm chooses price \(R\) to maximize \(R[1 - F(R)]\), and with \(V\) uniform on \([0,1]\) this gives \(R = \tfrac12\) and expected profit \(\tfrac14\). The dynamics emerge in a two-period model. A failed sale in period 1 reveals \(V < R_1\), so by Bayes’ rule the period-2 posterior is uniform on \([0, R_1]\) with \(F_2(V) = V/R_1\); the first-period price thus does double duty, affecting both period-1 sales and period-2 information. The firm maximizes

\[ \max_{R_1, R_2}\ R_1[1 - F(R_1)] + R_2[1 - F_2(R_2)]\,F(R_1), \tag{31.47}\]

solving the period-2 subproblem \(\max_{R_2} R_2[1 - F_2(R_2)]\) with posterior

\[ F_2(R_2) = \begin{cases} F(R_2)/F(R_1) & \text{for } R_2 < R_1,\\ 1 & \text{otherwise.} \end{cases} \tag{31.48}\]

The first-order conditions imply that the second-period price always lies below the first, and expected profit exceeds the one-period benchmark because the option to mark down raises the probability of an eventual sale. With a concrete uniform example, the two-period prices are \(R_1 = \tfrac23\) and \(R_2 = \tfrac13\) (since \(R_2 = R_1/2\) from the second-period first-order condition), against the one-period \(R_1 = \tfrac12\). The model abstracts from brand recognition and from contagion or network effects.

Thin markets and consumer heterogeneity enrich the price path. Suppose \(N\) customers inspect the good, each a shopper (valuation \(0\)) with prior probability \(P\) or a buyer (valuation \(V\)) with probability \(1-P\); a person learns which she is only upon inspecting. Three types coexist: customers, all who inspect; buyers, whose value equals \(V\); and shoppers, whose value is zero. The firm maximizes

\[ \max_{R_1, R_2}\ R_1(1 - F(R_1))(1 - P^N) + R_2\big\{(1 - F_2(R_2))(1 - P^N)\big\}\big\{1 - [(1 - F(R_1))(1 - P^N)]\big\}, \tag{31.49}\]

with period-2 density, by Bayes’ rule,

\[ f_2(V) = \begin{cases} \dfrac{1}{R_1(1 - P^N) + P^N} & \text{for } V \le R_1,\\[3mm] \dfrac{P^N}{R_1(1 - P^N) + P^N} & \text{for } V > R_1. \end{cases} \tag{31.50}\]

As \(P^N \to 1\)—almost everyone is a shopper—there is little information to be gleaned, so the two-period problem collapses to two independent one-period problems and prices are roughly constant. When \(P^N\) is small, prices start high and fall rapidly as time unsold accumulates. The composite \(P^N\) thus stands in for search cost and information. Observable price–quantity patterns follow from three primitives: the number of customers \(N\), the proportion of shoppers \(P\), and the firm’s prior on \(V\). Where prices fall quickly, the chance the good goes unsold is low; a high initial price signals a low \(P^N\)—few shoppers—and so predicts a likely sale. Greater prior dispersion raises the expected price for a given mean but, through longer shelf time, can lower expected revenue. The more obsolescence-prone (“fashion”) the good, the more anxious the seller and the steeper the markdowns; “classic” goods carry higher initial prices that are less sensitive to inventory. A constant discount rate is irrelevant to the pricing condition, unlike an increasing obsolescence rate, and for a non-unique good the solution reduces to the one-period problem. Costs themselves fall through three distinct channels worth keeping separate: economies of scale, \(c(\text{units})\); economies of scope, \(c(\text{types of products})\), typically via knowledge transfer; and the experience effect, \(c(\text{cumulative output over time})\), a superset of scale economies.

The Internet sharpened the search question. Conventional wisdom held that lower search costs intensify price competition, but the analytical literature complicates this. Lal and Sarvary (1999) distinguishes digital product attributes, communicable over the Internet, from nondigital attributes that are not, on a demand side where consumers vary, and a supply side where firms operate both traditional and Internet stores. Monopoly pricing can survive—prices stay high and search is discouraged—when a high proportion of consumers are Internet users, nondigital attributes are not overwhelming, consumers favor familiar brands, and shopping is destination-driven; stores serve to acquire customers while the Internet retains loyal ones. Kuksov (2004) shows the design margin matters: for products whose design cannot be easily changed, lower search costs raise price competition, but for products whose design is flexible, lower search costs induce firms to increase differentiation, which softens price competition, lowers social welfare, and raises industry profits—so the welfare effect of cheaper search hinges on whether firms can respond by redesigning. Salop and Stiglitz (1977) supplies the foundational model of costly search underlying this stream.

31.14 Pricing and Promotions

Pricing promotions are among the most heavily studied phenomena in marketing, and the analytical lens reframes “loyalty” in the language of information: an uninformed consumer behaves like a loyal one, and an informed consumer like a non-loyal switcher. The strategic questions are whether to run everyday-low- pricing or high–low pricing, and how to design short-term discounts—trade deals to the channel, and consumer promotions such as shelf-price discounts (used by everyone) and cents-off coupons (used by consumers whose time is relatively cheap).

The decomposition of what a price cut actually does is well established. Gupta (1988) attributes the bulk of the measured sales response to brand switching (about 84% of the effect), with purchase acceleration (about 14%) and quantity increases (about 2%) accounting for the rest, and finds the elasticity of short-term price changes to be an order of magnitude larger than other elasticities. Beyond the measured effects, promotions can drive general trial, encourage consumers to hold inventory and thereby raise consumption, lift sales of complementary products, and produce small store-switching effects—with an asymmetric pattern in which stronger brands benefit more, except against store brands. Against these benefits stand persistent costs: consumers come to expect future promotions, their reference price ratchets down, their price sensitivity rises, and a post-promotion dip follows as stockpiled demand is repaid.

Trade discounts—short-term discounts offered to the channel rather than the consumer—incentivize retailers to push the product and capture the sales force’s attention, but they may not be passed through to consumers, they invite forward buying that disrupts production planning, they complicate demand forecasting, and they breed an expectation of future discounts that becomes a cost of doing business. Scanback arrangements, which tie the discount to verified retail sales, raise pass-through. Pass-through is higher when consumer elasticity is higher, the promoting brand is stronger, the demand function has a favorable shape, and promotions are infrequent. On shelf-price discounts, Raju, Srinivasan, and Lal (1990) shows that a stronger brand can discount infrequently precisely because weaker brands cannot predict when it will promote and so must promote more often to defend their position.

Coupons illustrate the design subtleties. Little over 1% of coupons are redeemed annually, their price-discrimination power has eroded with their ubiquity, and the sales lift required to make free-standing-insert coupons profitable is often unattainable. Coupon design—expiration dates and distribution method—therefore matters: stronger brands should set shorter expiration windows, because a larger share of their loyal base will use the coupon regardless; in-store distribution dominates through-package and targeted distribution on average. Package coupons embody an acquisition–retention trade-off across three types: peel-off coupons are used by many but yield the lowest firm profit; in-pack coupons attract fewer first-period buyers; and on-pack coupons, redeemed on a subsequent purchase, are typically the best approach. The summary verdict is that trade and consumer promotions are both necessary, that consumer promotion should lean toward package coupons rather than shelf-price discounts or newspaper coupons, and that the strong interaction between advertising and promotion remains an open research frontier.

It helps to organize discrimination by degree: first-degree discrimination prices on individual willingness to pay, second-degree on quantity, third-degree on observable membership, and fourth-degree on cost-to-serve.